R&D Units - Funding 2020-2023

Procurement of goods and services

-

Procurement of goods and services (AQ) and other current expenses directly related to the objectives of the funding (e.g., laboratory consumables, procurement of instruments, goods for common use directly related to the pursuit of the objectives of the funding, among others).

-

Similar to the submission of expenses with intra-Community VAT, expenses related to services with income tax withheld must also be presented on two lines, since payment of this tax occurs at a different time from payment for the service. Therefore, the columns relating to payment should include information relating to the payment of income tax to the State (see Expense Submission Manual, page 25, example 4).

In view of this, when income tax is withheld, the expense for this green receipt must be presented on two lines. One line for the amount received by the service provider and another line for the delivery/payment to the AT of this income tax withheld by the institution.

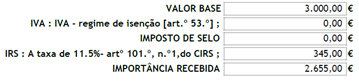

1st Example: without VAT and with income tax

Amount paid to the service provider = 2,655.00

Amount paid to the Tax Authority (Article 101(1)(c) of the CIRS) = 345.00

The amount that should appear in cell "D. Expense Amount" is the Base Amount of the receipt.

In the first line (amount paid to the service provider), the allocation rate should be calculated as follows:

Allocation rate (1st line) = Amount paid to the service provider / Base Amount = 2,655.00 / 3,000.00 = 88.50

Imputation rate (2nd line) = Amount paid to the AT / Base Amount = 345.00/3,000.00 = 11.50

The sum of the two imputation rates must equal 100. Thus, we have 88.50 + 11.50 = 100.

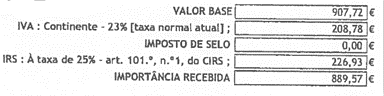

2nd Example:with VAT and with income tax

Amount paid to the service provider = Base Amount + VAT – IRS = 907.72 + 208.78 – 226.93 = 889.57

Amount paid to the Tax Authority (AT) (Article 101(1)(b) of the CIRS) = 226.93

The amount that should appear in cell "D. Expense Amount" is the sum of the Base Amount + VAT = 907.72 + 208.78 = 1,116.50.

In the first line (amount paid to the service provider), the allocation rate should be calculated as follows:

Allocation rate (1st line) = Amount paid to the service provider / (Base Amount + VAT) = 889.57 / 1,116.50 = 79.6749

Imputation rate (2nd line) = Amount delivered to the AT / (Base Amount + VAT) = 226.93/1,116.50 = 20.3251

The sum of the two imputation rates must equal 100. Thus, we have that 79.6749 + 20.3251 = 100.

-

The most correct way would be to submit the invoice in the first line and the corresponding credit note in the second line, providing as complete a description as possible in both and correlating the two.

-

In the case of percentage allocations of an expense, a framework and justification for the percentage allocation must be provided, allowing for a clear and accurate analysis of the expense.

-

Subscriptions for access to publications, databases (among others) must be collective in nature, i.e., accessible to the entire UID Unit and not on an individual basis for each researcher. They must be aligned with the scientific objectives of the funding and, consequently, contribute directly and exclusively to the implementation of the Unit's scientific activity plan.

-

No. Only expenses supported by invoices, or equivalent documents, issued in the name of the beneficiary (main or participating Management Institution) in accordance with Article 29 of the Value Added Tax Code (CIVA) and receipts or equivalent discharge documents, with all the defined tax requirements being met, in particular Article 36 of the CIVA, and proof of actual payment being provided through the financial flow associated with the document.

-

Provided that the direct link with the pursuit of the project's objectives is safeguarded and a framework for this is established, the expenditure will be eligible. However, it should only be allocated in proportion to the years of funding in force and not for the entire 10 years.